Personal debt is a nearly universal experience in the United States, but each generation carries this burden in a different way. The type and amount of debt someone holds can depend on their stage of life and financial circumstances. Recent surveys reveal that some generations are more likely to carry non-mortgage debt, while others shoulder the highest overall balances or feel the heaviest burden of unmanageable personal debt.

Gen Z, the youngest adult generation, hasn’t had as much time to borrow, but they’re entering adulthood under unique financial pressures and technology-heavy modern credit markets.

Which Generation Has the Most Debt?

There may not be a single generation that clearly holds the most debt.

- Baby Boomers and Gen Xers may be more likely to carry larger balances tied to mortgages and credit cards.

- Millennials tend to be the most burdened by student loans.

- Gen Z is a little different. The overall individual debt balances may be lower for this group, as younger people have had less time to borrow, after all. But data suggests Gen Z has entered adulthood with more personal debt than expected.

A round-up of debt-related stats by generation hints at the complex nature of this question.

Data from Go Banking Rates indicates that Gen Z carries an average of $94,101 in personal debt. That’s higher than the averages it reports for Millennial and Gen X individuals, which are both less than $60,000.

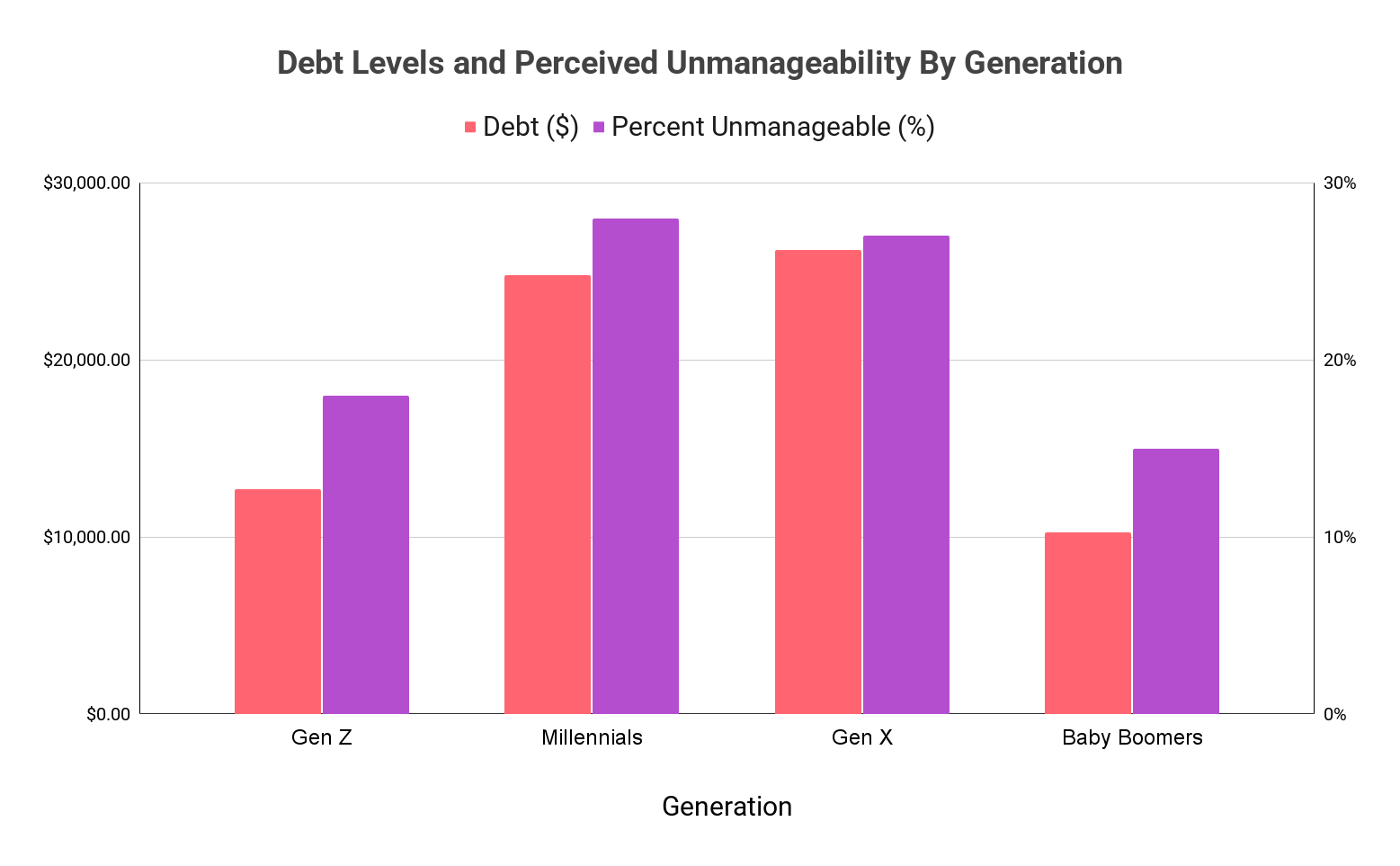

When it comes to non-mortgage debt, Gen X may have more. Analysis of more than 500,000 anonymized credit reports by LendingTree researchers indicated an average median non-mortgage debt for each generation of:

- Gen Xers: $26,207

- Millennials: $24,810

- Gen Zers: $12,715

- Baby Boomers: $10,272

Results from an Experian survey indicated how people in each generation felt about their personal debt level. Here’s the percent of each group that said their unsecured debt was “unmanageable”:

- Millennials: 28%

- Gen Xers: 27%

- Gen Zers: 18%

- Baby Boomers: 15%

Though fewer Gen Z borrowers describe their debt as “unmanageable,” the rising use of credit products means their financial relationship with debt is taking shape quickly. This emerging pattern raises questions that extend beyond the amount of debt Gen Z holds, such as why they’re accumulating it and what that reveals about their unique financial challenges.

Why Is Gen Z in So Much Debt?

Gen Z’s outsized debt isn’t driven by one cause but by a mix of tough economic conditions and changing financial habits.

Inflation and rising costs

The Bureau of Labor Statistics reported a year-over-year increase in the Consumer Price Index for the cost of all goods of 2.7% as of July 2025. Inflation and price increases are hitting Gen Z hard, and the majority of younger people say their monthly expenses are higher than anticipated in categories like:

- Groceries (63%)

- Rent and utilities (47%)

- Dining out (42%)

Higher prices may be driving Gen Z to live outside of its means by using revolving credit like credit cards to cover the dinner check or weekly grocery run.

Stagnant wages

The Atlanta Fed’s Wage Growth Tracker shows an overall decline in 3-month moving average median wage growth from July 2022 through July 2025. In July 2022, overall unweighted wage growth for hourly positions was around 6.7%. Three years later, it was close to 4%.

Without stagnant wages, many Gen Zers are struggling to keep pace with the monetary requirements of daily life.

Doom spending

Doom spending means spending money, often on non-essentials, as a way to deal with stress and anxiety.

Little treat culture, which has normalized multiple expensive beverages or takeout purchases weekly, is a potential example. More than half of Gen Zers say they purchase treats once a week or more to reduce stress or celebrate small wins — and almost 60% note this leads to overspending.

Regular credit usage

All these factors have contributed to Gen Z’s early adoption of credit. By 2024, Gen Z carried an average of $2,834 in credit card debt. It might not sound like much, but that’s 25% more than Millennials carried at the same age.

Credit cards and other revolving credit options, including buy-now, pay-later services, are deeply ingrained in modern spending processes. They’re embedded in carts, pushed as more secure ways to shop and marketed with rewards and loyalty programs, increasing the draw for Gen Z.

How Debt Is Affecting Gen Z

From missed payments to mental health concerns, the impact is multifaceted. Effects include:

- Increases in delinquencies

- More financial instability

- Delayed financial goals

- Mental health strain

- Reliance on alternative financial products

Increases in delinquencies

Consumer credit data from the New York Fed noted that 15.3% of Gen Z credit card holders had maxed out their limits in 2024 — a higher rate than any other generation. Maxed limits and rising payment delinquency are a concern for people under 40, including Gen Z.

More financial instability

In a Deloitte survey, 73% of Gen Zers reported living paycheck to paycheck, leading to greater reliance on short-term and revolving debt products.

Delayed financial goals

Again, the majority of Gen Zers said it was difficult to save. Other financial goals many struggle with as they face rising costs and debt include paying down unsecured debt, living on a single income, and buying a home.

Mental health strain

More than 40% of Americans say money struggles negatively impact their mental health. Gen Z, like other generations, faces anxiety, stress, loss of sleep, and other health impacts due to personal debt.

How Gen Z Is Coping

As debt challenges mount, proactive Gen Zers find ways to adapt and gain control over their finances.

Use of alternative payment methods and related tools

BNPL platforms are a popular way to spread out costs to make purchases more accessible. But they go beyond a debt opportunity for Gen Z. Many are evolving into credit-building or money management tools.

- Sezzle’s Sezzle Up program gives shoppers the option to report payments to the credit bureaus, helping users establish a positive credit history.

- Klarna offers budgeting and spending insights through its app.

Splitit lets credit card holders make interest-free installments on purchases using their existing credit card limit, reducing potential debt costs while maximizing card reward benefits.

Proactive and tech-savvy financial management

Many Gen Zers are turning to budgeting apps and digital wallets to stay on top of their finances. Around 55% of this generation uses advanced budgeting tools. That’s more than in any other age group.

It’s not surprising that the generation that grew up with smartphones is implementing these tools into money management. Some alternative financial products like BNPLs are taking note of this and have developed budgeting tools and financial resources to empower young consumers and encourage responsible spending. These smart tools help compare prices, create watchlists, set budgets, and most importantly, create financially literate consumers.

Working to improve financial literacy

The tech-savvy generation is often willing to admit when it needs to hit the books — or the YouTube channels. Many turn to tools like Mint and YNAB for more than tappable budget management. They read articles, watch videos, and otherwise seek out advice on handling money and planning for the future.

Is Gen Z More Financially Savvy?

While Gen Z faces rising debt and financial pressures, they may be better prepared to deal with these challenges than previous generations were. Many younger adults are adopting digital tools to track spending, seeking financial knowledge early, and experimenting with ways to build credit.

Non-traditional credit-building programs, such as Sezzle Up, and the overall flexibility of modern payment platforms, including buy now, pay later platforms, can also help Gen Z make the most of the resources they have.

While Gen Zers aren’t immune to personal debt risks, their financial journey is only just starting. They have a long way to go, and it seems they have a lot to prove to their older counterparts.